A Complete Guide to Risk Management in Insurance

Sharlyn Bedi | 30th March, 2025

9 min reads

Sharlyn Bedi | 30th March, 2025 | 9 min reads

The potential red flags to look out for in the growth and regulation of the Indian insurance sector vary from fraudulent claims and misrepresentation to regulatory problems and operational inefficiency. According to an expert, it has been shown that about 10-15% of claims, based on behaviors of fraud, cost insurance companies almost INR 900 Crores per annum. Furthermore, more than 60% of insurers are reporting a rise in fraud cases, a scenario that cannot be ignored, urging the industry to take timely decisions on implementing auditing and risk management measures.

To put it another way, insurers, leveraging AI, machine learning, and predictive analytics, will be able to better identify fraud, meet compliance benchmarks, and streamline their operations. As new risks develop, efficient risk management should not be something to think about but a necessity. Established in this guide are key risks and challenges, along with the technologies and best practices in risk management for the Indian insurance sector.

What is Risk Management in Insurance?

Risk management in insurance involves identifying, assessing, measuring, and thereby being utilized to mitigate risks that can negatively affect the operations and financial performance of an insurance company. Risk management in insurance is fundamentally concerned with reducing uncertainties, effectively averting massive financial losses, and thereby ensuring fairness for policyholders. Risk management can enhance decision-making by insurers, ensure compliance with regulatory guidelines, and assist with the building of the company in the market.

Importance of Risk Management in the Indian Insurance Sector

A few of the most important reasons propounding active practice of risk management in insurance industry in India include:

Financial Protection: Proactive identification and mitigating risks result in the prevention of heavy financial losses due to fraud-oriented claims, underwriting errors, and operational inefficiencies.

Regulatory Compliance: Due to the highly regulated nature of the Indian insurance sector, a well-structured risk management process is required in order to comply with the dynamically changing laws and standards without risking legal penalties or operational licenses.

Operational Efficiency: This is achieved by streamlining processes, reducing duplicative practices, thus realizing great operational efficiency, leading to a cost reduction and enhanced service delivery.

Customer Trust: A company exhibiting good risk management helps cultivate the trust of customers since it reflects the company's stability and commitment towards them.

Market Competitiveness: Efficient risk management practices will permit insurers to conform to changes in the market environment, develop innovative products, and successfully compete, resulting in a competitive edge over their rivals.

Keeping this in mind, it is evident that there is no less than an urgent need for reinforcing risk management in the domain of Indian insurance. Risk management thus remains the keystone that guarantees the ideal functioning of the market: financial, regulatory, operational, and customer confidence.

Types of Risks in Insurance

Effective risk assessment and mitigation are key pillars that hold the insurance industry on the road to prosperous financial results and customer trust. However, insurers face a plethora of risks that may inhibit profitability and catalog the workability or compliance. In light of these challenges, risk management takes over, held by a functional integration of technology and regulatory obligations. Some of the most common risks associated with insurance are as follows:

Claims Fraud Risk

Claims fraud is one of the major causes of financial loss that eventually leads to increased premiums for honest policyholders. The types of fraud include fake claims, exaggerated claims, self-sabotage, the assumption of another's identity, and duplicitous claims filed with several insurers. As with insurers, any fraudulent act creates a risk of increased litigation, damage to the insurer's reputation, and delays in the settlement for legitimate policyholders. To manage fraud, the insurance carrier often relies on AI for fraud detection, tamper-proof records on the blockchain, and biometric verification to ensure the claim being filed is genuinely substantiated.

Underwriting Risk

Incorrect risk assessment during underwriting processes may lead to poor financial performance and inefficient pricing. Various factors, including adverse selection and moral hazard within fluctuating markets, may lead to bad underwriting decisions, higher claim payouts, and loss ratios. Irregularities in underwriting will lead to customer dissatisfaction, surrender of policies, and increased backlash from regulatory authorities. Insurers are adopting predictive modeling, AI-based risk scoring methodologies, and live monitoring via the IoT to strengthen the prospect of underwriting.

Regulatory & Compliance Risk

The threat of non-compliance with strict yet just regulatory frameworks is maximum; nevertheless, it poses major challenges to an insurer's business and reputation. The standards required of many insurers include those in regard to solvency, KYC, AML, and data protection. Non-compliance will lead to reputational harm, surging operational costs, and increased monitoring. Risk reduction measures include automated compliance tracking, deep learning-based KYC, safe digital records for transaction transparency, and auditing processes.

Information Security & Data Risk

With the emergence of new digital platforms, insurance companies have become prime targets for cyber threats. These can include data breaches, ransomware, phishing, and cloud vulnerabilities. A single cybersecurity breach may cause potential financial losses, legal consequences, and customer mistrust. Strengthened data protection, on one hand, encompasses the use of strong encryption, real-time detection and response against threats, multi-factor authentication, and the adoption of a zero-trust security framework to alleviate exposure to cyber risks.

Operational Risks

Internal inefficiency, human errors, and IT failures can potentially derail insurance functions, resulting in delayed claims, regulatory inquiries, and increased administrative costs. Delayed or incorrect claim settlement timelines, unavailability of the system, employee fraudulent activities, and dependency on third parties increase operational risks. Insurers mitigate these risks through automated claims processing or robotic process automation (RPA) in workflow optimization and improved governance, either through stricter internal policies or through a risk assessment of all third parties before outsourcing services.

Market & Financial Risk

Economic shifts, changes in interest rates, and global financial crises all affect insurers' ability to remain solvent and fulfill claims obligations. The people involved and how they react to a market-related crisis determine the outputs from investment portfolios, delays in returns due to liquidity shortages, and changes in foreign exchange for international operations. Financial solvency is put into question; regulatory breaches may often follow, and in the worst-case scenario, even insolvency may materialize. To mitigate these risks, insurers follow investment diversification, capitalization of assets, and hedging to insure against market uncertainties.

By addressing such types of risks with the requisite technology, data-driven decision-making, and proactive compliance measures, insurers can strengthen operational efficiencies, sharpen fraud detection, and assure long-term financial stability.

Secure your business with smarter risk management—Sign up today!

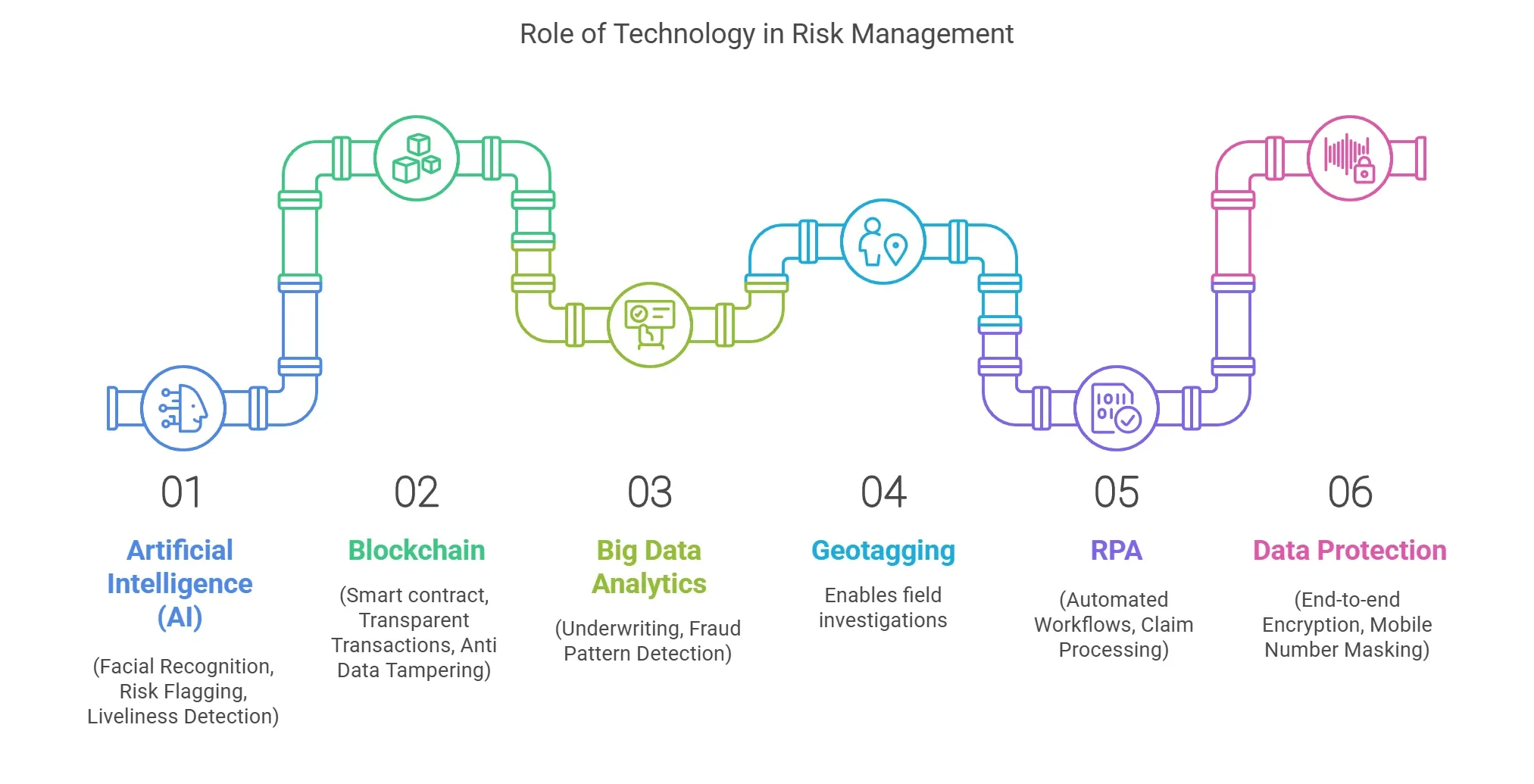

Role of Technology in Risk Management

The insurance sector is undergoing a transformation as new technologies are being introduced for offering risk management, fraud control, and compliance with regulations. New technologies such as artificial intelligence (AI), blockchain, IoT, and big data analytics enable insurers to operate in a systematic way with maximum risk containment.

Such technological innovations are becoming an integral part of operations, which help control losses due to financial issues, resulting in a better customer experience and decision-making process.

Fraud Detection in Insurance Claim Processing: Insurance fraud remains one of the most significant threats to the insurance sector. The AI-based tools used for detecting fraud operate on the fundamental principle of accessing historical data, detecting suspicious patterns, and real-time flagging of high-risk claims. The machine learning models are fed with past experiences of fraudulent cases and they learn continuously, improving their accuracy to some extent independently. Insurers also implement predictive analysis on claims history, social media activities, and policyholder behavior, to detect potential fraud before payment has been made.

Underwriting And Policyholder Risk Control: In recent years, the underwriting processes have been transformed due to the use of AI-enabled risk evaluation models that rate policyholders based on multiple risk parameters. Traditional underwriting used to happen through manual assessment but modern underwriting now combines both AI and big data and analyzes customer history, health records, financial stability, and behavioral data. Such automation eliminates human bias, speeds up the approval process, leads to quicker underwriting, and ensures fair premium pricing based on actual risk levels.

Field Investigation: To validate claims, field investigations become a crucial factor in validating claims, especially in motor and health insurance. Digital tools such as geotagging, and automated report generation enable field investigations to be done efficiently. Facial recognition and image analysis backed by AI can ascertain whether the accident site is the same as what is reported in the claim, identify discrepancies between the two, and authenticate evidence submitted to make the utmost reduction in fraudulent claims.

Video KYC for Fraud Prevention: After the introduction of stricter regulatory guidelines on Know Your Customer (KYC), video KYC is gradually becoming a strong weapon for preventing frauds. AI-powered liveness detection, facial recognition, and OCR can enable the insurance claim and premium payments process to verify the identity of policyholders remotely. The introduction of Video KYC would confirm all frauds such as establishing fake identities, document forgery, and impersonation, therefore enhancing the onboarding process.

Digital Verification & AI-Powered Risk Assessment: Insurers today use AI-based document verification, biometric authentication, and digital signatures to fortify customer onboarding and claims processing through improved risk assessment. AI tools compare customer-provided information against official databases in search of discrepancies. Risk-scoring models analyze variables such as income, spending behavior, and previous claims history to categorize policyholders by risk level.

Blockchain for Secure Transactions: Blockchain technology is redefining transparency within insurance transactions. By creating an immutable, decentralized ledger for storing policy contracts, claims history, and transactions, blockchain protects against the tampering of data and unauthorized alterations. Smart contracts help facilitate and highlight automatic settlements of claims based on some pre-set criteria, allowing for the minimization of delays and an increase in trust.

Cybersecurity Measures for Data Protection: Since insurance companies are dealing with highly sensitive information on millions of their customers, causes of cybercrime such as ransomware, phishing, and data breaches must be dealt with firmly. Artificially intelligent threat-detection applications, multi-factor authentication, and end-to-end encryption help shield the insurance company's databases. Insurers are also adhering to a zero-trust security model and real-time threat monitoring to recognize and mitigate the challenges of the cyber threat landscape.

Robotic Process Automation (RPA): RPA facilitates repetitive daily tasks such as record data entry, verifying documents, and fraud detection. This would decrease the need for manual labor, leading to an accelerated pace of claim processing, faster reduction in errors, and allowing human resources to focus on other complex investigations that require a detailed analysis.

Big data and Predictive Analytics forecasting risks: Predictive analytics empowers insurers to analyze numerous pieces of structured and unstructured data to identify risks that are likely to occur. By using artificial intelligence algorithms, insurers can anticipate the behavior of a policyholder, ascertain the probability of a future claim, and hunt down the fraud patterns. This risk-based intervention provides room for further adjustments to companies' pricing models, improvements to underwriting practices, and expanded insurance products that allow market differentiation in an ever-evolving insurance sector.

Such technologies can fundamentally shift traditional insurance practices and offer integrated risk mitigation, along with regulatory compliance and customer satisfaction improvement.

Sign up and upgrade your claims investigation process today!

Objectives of Risk Management in Insurance

Insurance risk management is of major importance in the context of protecting financial stability, ensuring regulatory compliance, and building customer trust. A properly defined risk management strategy would help all insurers deal with uncertainties, curtail fraudulent activities, and improve the operational process. The goals of insurance company risk management include:

Prevent Financial Losses: Fraudulent insurance claims, underwriting errors, and inadequate risk assessment can cause significant financial losses. With AI for fraud detection, predictive analytics, and real-time monitoring systems, insurers can reduce unnecessary payouts and safeguard their capital.

Insurance Legal Compliance: Insurance companies must follow strict regulatory requirements, such as Anti-Money Laundering (AML) laws, Know Your Customer (KYC) rules, and other industry regulations like IRDAI. Automated tools for compliance monitoring typically track transactions, identify potentially suspicious operations, and create reports according to regulations to avoid paying fines.

Improve Claims Accuracy: Inaccurate claims processing can lead to delays for customers, disputes with them, or dissatisfaction with products. The use of AI should enable claims automation to verify claims accurately and thus reduce the rate of fraudulent claims and speed up payment for legitimate claims. This, in turn, contributes to enhancing the insurer's reputation and solidifying the base of returning customers.

Enhance Policyholder Trust: Transparency and fairness in the risk management purview would build trust. Digital verification tools, automated underwriting, and AI-enabled fraud prevention ensure that customers are charged fairly, are rapidly compensated on claims, and that their funds are secure, which will therefore boost confidence in the insurer.

Improve Operational Efficiency: Automation of underwriting, claims processing, and fraud detection improves several factors: by eliminating additional manual workload, speeding up processing, and overall efficiency improves further. Robotic Process Automation will act as an enabler to deal with huge inflations of data with minimal errors, which will lead to reduced administrative costs.

Mitigate Emerging Risks – The insurance industry faces evolving risks, including cyber threats, regulatory changes, and economic fluctuations. Advanced analytics, machine learning, and real-time data monitoring help insurers identify emerging risks and adapt their risk management strategies proactively.

Enhance Decision-Making with Data Analytics – Data-driven decision-making enables insurers to refine pricing models, assess market trends, and identify high-risk policyholders. By leveraging AI and big data analytics, insurers can make informed decisions that improve profitability and risk assessment accuracy.

A comprehensive risk management framework ensures that insurers can proactively manage risks, protect their financial stability, and provide customers with reliable and secure insurance solutions. Through technology-driven solutions and a strategic approach to risk mitigation, the insurance industry is evolving to become more resilient and efficient in handling uncertainties.

Detect fraud faster with AI-powered field investigations. Sign up today!

Challenges in Risk Management for Insurers

The insurance industry faces several evolving challenges in risk management, making it essential for insurers to adopt advanced strategies and technologies to mitigate risks effectively. Some of the key challenges include:

Rising Claims Fraud – Fraudulent claims continue to be a significant challenge for insurers, leading to financial losses and impacting policyholder trust. Fraudsters use fake documentation, staged accidents, and identity theft to manipulate claims, making it crucial for insurers to strengthen fraud detection mechanisms.

Complex Regulatory Requirements – Insurance companies must comply with stringent regulations, including Anti-Money Laundering (AML), Know Your Customer (KYC), and data protection laws. Navigating these complex compliance frameworks requires robust monitoring and automated solutions to avoid legal penalties and reputational damage.

Cyber Threats in Insurance – With insurers handling vast amounts of sensitive customer data, cyber threats such as ransomware attacks, data breaches, and phishing attempts have increased. Ensuring data security through advanced encryption, real-time threat detection, and multi-layered cybersecurity measures is critical.

Manual & Delayed Risk Assessments – Traditional risk assessment processes are often manual, time-consuming, and prone to human errors. Delayed assessments lead to inaccurate underwriting decisions, inefficient claims processing, and increased exposure to high-risk policyholders.

High Operational Costs – The cost of maintaining multiple risk management tools, manual processing, and regulatory compliance can strain insurers’ profitability. Automating risk assessment, fraud detection, and compliance monitoring can significantly reduce operational expenses.

Identity Verification in minutes with automated Video KYC. Book a Demo now!

Manage All Insurance Risks in One Platform – Kriyam’s AI-Powered Risk Intelligence

Why struggle with multiple risk management tools when you can streamline all risk-related processes in one AI-driven platform? Kriyam provides an all-in-one solution designed to enhance fraud detection, automate compliance, and improve operational efficiency.

Key Features of Kriyam’s AI-Powered Platform:

- Easy Claims Processing – Easy workflows for claims processing, document verification etc.

- Automated Video KYC & Digital Verification – Enhance customer verification with AI-based liveness detection, facial recognition, and document authentication.

- Regulatory Compliance Monitoring – Ensure full adherence to legal and industry regulations with automated reporting and real-time compliance tracking.

- Field Investigation & Risk Intelligence Solutions – Geotagging, Real-time Tracking & Automated Case Summary.

- Data Protection – Secure sensitive policyholder data with advanced encryption & masking techniques.

How Kriyam Helps Insurance Companies?

By integrating AI-powered fraud investigation, insurers can reduce fraud, improve claims accuracy, and ensure full regulatory compliance in a single, unified platform. Kriyam empowers insurers to stay ahead of risks while enhancing policyholder trust and operational efficiency.

Final Thoughts

Risk management in insurance is no longer an option—it is a necessity in an industry facing rising fraud, regulatory complexities, and operational inefficiencies. Insurers must adopt AI-driven solutions, automation, and advanced analytics to proactively mitigate risks, ensure compliance, and enhance policyholder trust. By using platforms like Kriyam’s AI-powered risk intelligence, insurers can streamline risk management, improve fraud detection, and secure long-term sustainability in an increasingly digital landscape.

People Also Ask

1. What is risk management in insurance?

Risk management in insurance involves identifying, assessing, and mitigating financial and operational risks to minimize losses, ensure compliance, and improve overall efficiency.

2. Why is risk management important in the insurance sector?

It helps insurers prevent fraud, enhance underwriting accuracy, comply with regulatory requirements, and build trust with policyholders by ensuring fair and transparent processes.

3. What are the common risks faced by insurers?

Insurers face various risks, including claims fraud, underwriting errors, regulatory non-compliance, cyber threats, and high operational costs.

4. How can technology help in insurance risk management?

AI, machine learning, and automation help insurers detect fraud, streamline underwriting, automate compliance monitoring, and improve claims verification through digital tools.

5. What is the role of AI in insurance risk management?

AI plays a crucial role in fraud detection, customer verification (Video KYC), claims processing, risk assessment, and regulatory compliance, reducing manual errors and improving efficiency.

About the author

Sharlyn Bedi

Junior Content Strategist

Sharlyn Bedi | Junior Content Strategist

A passionate writer with a knack for automation and process optimisation. Through clear, actionable insights, her content is best for leaders to stay updated on latest trends on technology and automation.

Interests: Business Automation, Process Optimization, Digital Transformation

Content Overview

Share

FEATURED

Insurance

5 Ways Agentic AI is Transforming Insurance Industry

This blog explores how pioneering insurers are leveraging Agentic AI to solve critical challenges—from eliminating claims backlogs to hyper-personalizing policies—while addressing ethical and operational hurdles.

Sreyan M Chowdhury

30th March, 2025